FIBR lending solutions for SMEs

Using better data to provide SMEs with fast, easy access to loans

Overview

FIBR was a digital lender that provided SMEs with fast and easy access to loans. They used technology to assess the creditworthiness of SMEs, including Open Banking and risk modelling. This allowed them to serve SMEs that would not have been approved by banks and traditional lenders.

Open Banking helped the team to assess businesses more quickly and accurately, making it possible to reach a larger market with fewer questions, and enabling their underwriters to make faster and more informed lending decisions.

What is Open Banking?

Open banking is a system that allows consumers to share their financial data with third-party financial services providers (TPPs) with their consent. This data can be used to provide a variety of new and innovative financial products and services.

ROLE

Lead Product Designer

UX and UI design (Web), workshop facilitation, team management, usability testing, research, branding,

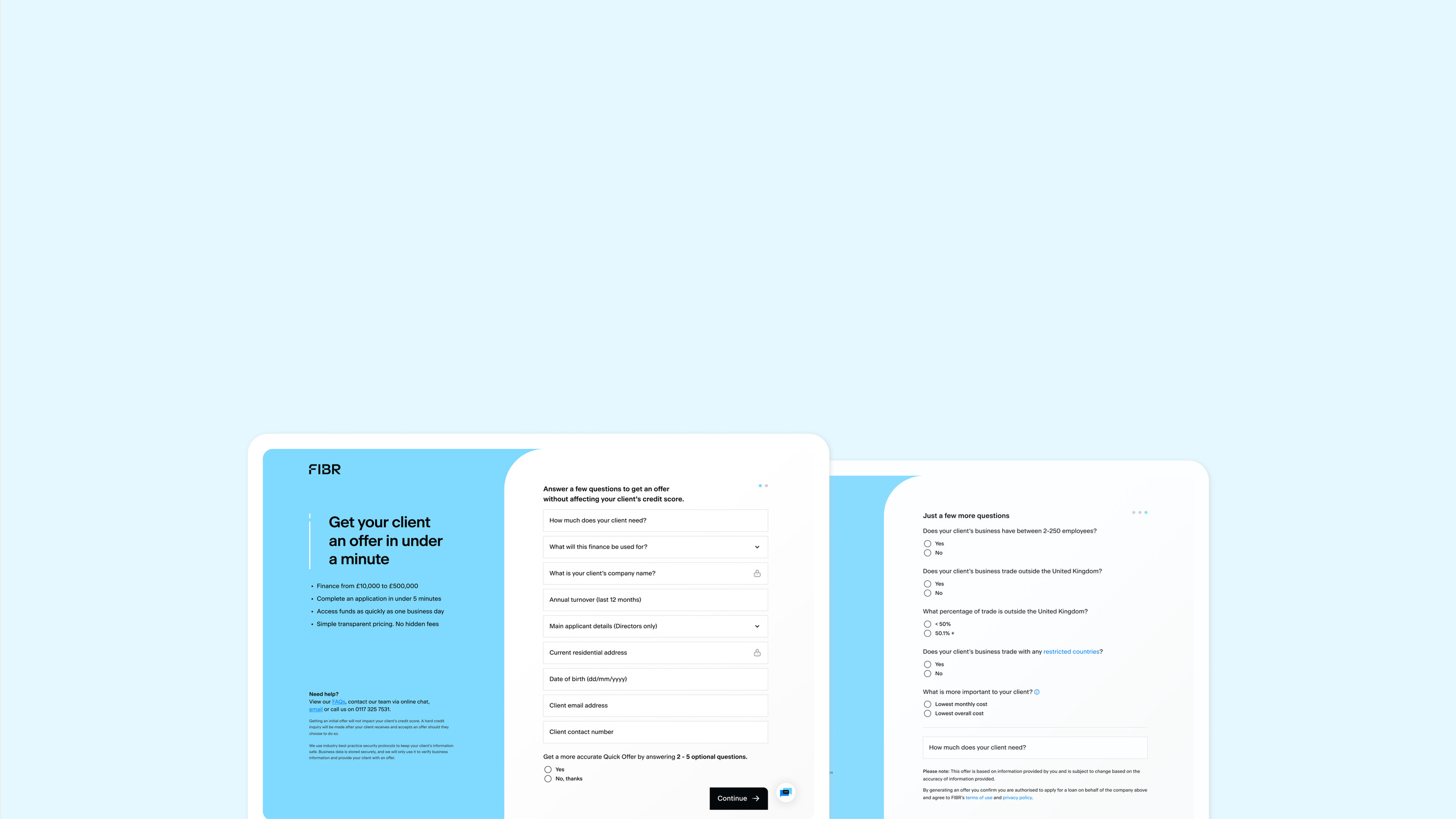

The problem

90% of FIBR's traffic and customer base came from broker partners. However, The company's initial web app was designed to service direct customers, and the onboarding flow did not allow brokers to complete the application up to a Firm Offer. This was due to two main factors:

The need for Open Banking, which required the end-borrower to connect their bank account. Brokers could not input further data without this connection.

Accounts were created using the end-borrower's details, which meant brokers could not complete applications on their behalf

(We also didn’t have a dashboard to allow brokers to track the status of applications…)

TL;DR

The solution

Within one campaign (9 weeks), our team rolled out a new, and significantly improved journey for broker applications, leading to a 24% increase in applications.

By enabling brokers to provide more data in a way that was familiar to them, we reduced the dependency on Open Banking connections. This improved the partner and end-user experience from the beginning of their journey with FIBR. Brokers understood the application better, and SMEs were more likely to connect their bank accounts after they had received a firm loan offer and were comfortable with the business relationship.

Solving Open Banking issues

As we dug deeper into the issues surrounding Open Banking, we found two main concerns:

Brokers couldn’t complete applications: Brokers were not able to connect their client’s bank accounts to get a firm offer.

Users were wary of Open Banking: General uptake of Open Banking is surprisingly low, and users were especially cautious when it came to sharing data from their business bank accounts.

Brokers couldn't complete the user journey because Open Banking was a must-have for firm offers.

To tackle this, we introduced a document upload feature.

This feature brought some important benefits:

A familiar experience: Our partners found it more user-friendly. They didn't have to worry about missing a step by not uploading all their customer's paperwork.

Access to key data: While not as automated as Open Banking, having early access to the data in these documents was a big help. It meant our operations and underwriting teams didn't need to follow up with extra questions when calculating loan eligibility and value.

By adding the document upload feature, we bridged the gap caused by the Open Banking requirement, making the journey smoother for our partners and users alike.

Users hadn't fully embraced Open Banking yet

(the uptake is pretty low, to be honest!)

The Open Banking step had proven to be a significant hurdle in our user journey, resulting in the highest dropout rate – only 7% of users had successfully completed this process. In response, we made a strategic adjustment: we moved the Open Banking step to the very end of the customer application process.

Moving the request for financial data to the end of the journey was aimed at enhancing the user experience and fostering confidence in our platform.

Making it easier for brokers to share offers with clients.

The previous discrepancies between our Quick Offer (calculated based on 10 data inputs) and the firm offer, which was determined using a significantly larger dataset, were reduced. Underwriters now had access to more comprehensive information, and brokers were able to obtain a firm offer before presenting it to their clients. This improvement meant no more having to explain why the final loan offer ended up being £50,000 less than the initial offer!

Brokers could now wait to share an “updated final offer” with their clients

Implemented automated email updates for brokers and saved time for our teams.

We noticed that brokers were constantly reaching out to our customer operations team for application status updates. To simplify the process, we set up automated email templates and a Salesforce email journey. This kept our partners informed about their applications and, in turn, saved our internal teams from sending 580 emails a month, along with 4 days of work monthly!

20+ email templates were designed across the FIBR user journey, with automation saving the customer success team hours in manual work

We didn't stop at just creating a good product; we made it even better.

One of the exciting changes we made was to streamline our risk modeling and underwriting processes.

For businesses that met specific criteria (like being in business for at least 2 years and seeking loans under £50K), brokers could take the fast track. This meant that by uploading all the necessary documentation, brokers could secure a firm offer for their clients in less than 24 hours. Once the paperwork was complete (and Open Banking was connected, of course), the funds were ready for the clients to access promptly.

Outcomes

90 minutes

Fastest application to offer time

+24%

Increase in broker applications

+4.4%

E2E conversion rate for fast-track apps

(against 1.6% for standard)

580 emails

saved from being sent manually every month

4 working days

saved per month for the ops team

Full case study coming soon (really)…